The capital of South Africa’s retirees is abysmal

By Bruce Cameron 30 March 2020

Alexander Forbes recently released the first major research on the financial survival of pensioners of retirement schemes in SA – and it does not make happy reading. This research was done before the Covid-19 outbreak and Moody’s downgraded South Africa. The situation now is likely to be far worse.

Alexander Forbes has examined a number of issues including retirement dates, choice of annuity (pension) and how much capital retirees have at retirement.

The big question, however, is: Do South Africa pensioners have enough money to last from the date of retirement until death? The answer for most is: no.

An actuary and a leader in retirement research, John Anderson, head of strategic development at Alexander Forbes, says many retirees are going to have cut back on spending and rely on others, such as children and relatives to survive.

If they are young and fit enough to work they need to get out there. This is a good option to supplement income if you can.

The older you are and the more ill you are, the less likely you are to find a job.

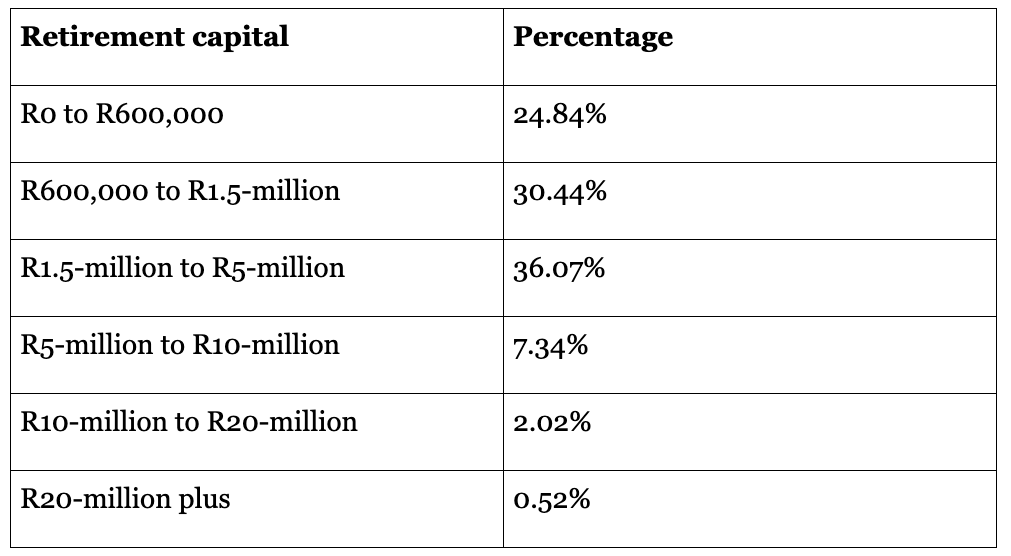

The survey is based on research on 11,594 pensioners, who retired between 1992 and 2018.

They retired with capital of R26-billion, an average of R2.2-million each.

But when you break down the “average” by age groups, the figures look very different.

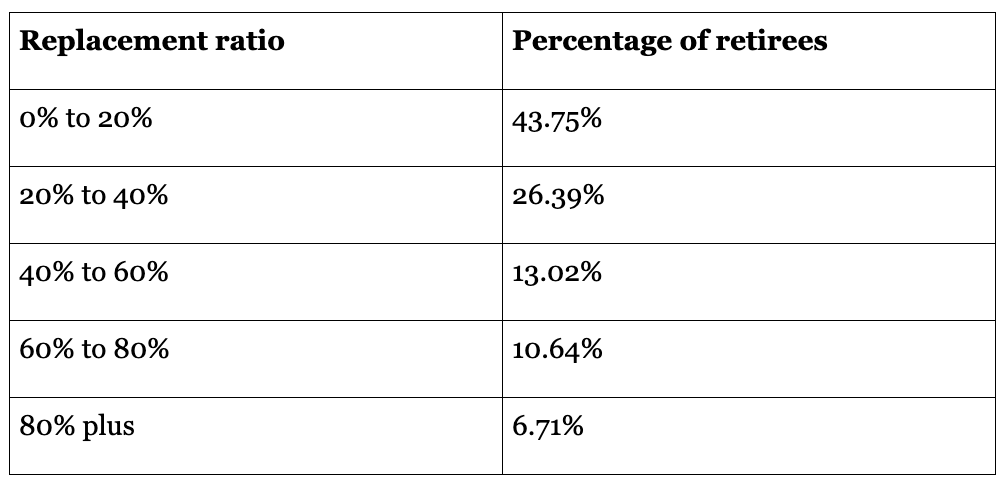

The next thing to look at is what are the replacement ratios. This means the percentage of your final paycheque without any add-ons such as car allowance or any other allowances.

Most retirement funds work on providing 75% of income after 40 years of service.

In other words, at least 85% of people did not save properly for retirement.

Anderson says the main reason for this is that people either started too late, or they cashed in their retirement funds when they changed jobs along the way.

While people may have additional savings outside of their formal retirement funds, this is not included in the study. That, however, is not likely to materially change the overall picture.

Other Alexander Forbes research shows that of more than one million contributing retirement fund members, of those who resigned, or were retrenched or fired in 2019, only 8.75% preserved their retirement savings. This is down from 11.5% in 2012. Most of this lack of preservation takes place when members are under the age of 50.

Anderson says during the current tough times in South Africa the number of people preserving retirement savings may shrink even further.

Once people reach retirement, they have to make a choice about retirement annuities. This is the money most will spend for the rest of their lives, and it is a critical choice.

The two main types of annuities (pensions) are: a traditional life assurance annuity where the pension is guaranteed and once you have made your choice you cannot change it; or what is called an investment-linked living annuity (Illa) where you make the investment choice and the underlying investments (with or without the aid of a financial planner). About 90% of pensioners chose Illas.

The basics of a traditional life assurance annuity are:

You pay a fixed amount for the annuity for life. Once bought it cannot be swapped.

-

The annuity can be linked to inflation or any other figure for a fixed annual growth. If you choose a level annuity, inflation will rapidly reduce your spending power.

-

There are other bells and whistles, such as making your partner one of the beneficiaries for life or guaranteeing an amount that will be paid as a pension to you or your dependants for a fixed number of years, whether or not you are alive.

-

You can also purchase a with-profit annuity which guarantees your initial pension. Future increases will depend on market conditions and how the underlying markets perform. Once an increase is granted it cannot be taken away in the future.

-

If you are on a “with-profit” annuity, rather than one tied to the inflation rate, under current conditions and how long they last, you will receive lower increases or zero increases in the years ahead but what you receive now is guaranteed.

The basics of an Illa are:

-

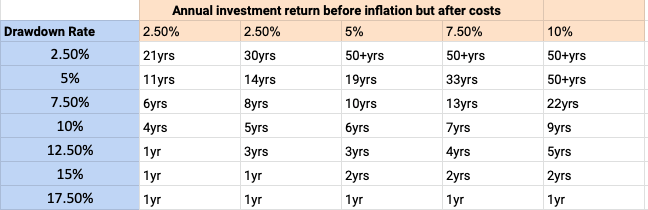

You can draw down between 2.5% and 17.5% of the capital amount annually. The lower the drawdown you chose the more likely your Illa will last. Here are tables recommended by the industry body, the Association for Savings and Investment South Africa (Asisa), based on what is called the “point of ruin”. This is the point at which your income has reached 17.5% and then starts to fall in rand terms:

What this graph shows is that if your drawdown rate is 2,5% and your investment return is 5% the moment you reach the “point of ruin” where your income will start declining in nominal terms (without the impact of inflation) Rand terms is at 30 years. The more you drawdown the closer to “ruin”: you will be. However if you say, select 12% as your expected rate of return you are unlikely to achieve. So while you may decide you want 12% return but you do not get it, you will actually reach you point of “ruin” far earlier. The point of ruin is not the end of your income flow but should only be reached later in your life.

Remember: These figures are estimates. This is why COVID-19, a harsh unexpected event, will bring the point of ruin forward very quickly depending on how long it and the consequent economic circumstances last.

-

You decide on the underlying investments either on your own or with help of a financial planner. This is where many investments have failed over the years as the underlying investments were too high risk for an income-based source of money.

-

You can leave what is left of your Illa to dependants. The problem, however, is that very few will die with much left in the retirement funds.

-

The average initial income drawdown rate of Asisa is 7% and that of Alexander Forbes was 6.42% in 2019. The Asisa rate has been dropping, but the Alexander Forbes rate has been going up.

Anderson says these figures do not reflect the true story as they are based on averages and skewed by pensioners with large retirement capital (who typically have much lower drawdown rates).

He says other research in the survey shows that of the pensioners surveyed at the time of their retirement there were:

-

Between around 70% and 77% with capital of less than R1,500,000 with drawdown rates higher than 5%.

-

Between 24% and 36% with capital of less than R1,500,000 with drawdown rates higher than 7.5%.

-

Close on 25% with capital of less than R600,000 have drawdown rates higher than 10%.

Anderson says this means that the averages hide the fact that people who have saved enough for retirement have very low drawdowns, while people who have saved too little for retirement have high drawdowns.

It also hides the fact that for those pensioners who took up Illas over the last 20 years, in many cases their drawdown rates have been increasing – and this is expected to be affected by Covid-19 with the resulting market impact and the downgrade by Moody’s, which in effect means we will be removed from international passive funds.

Anderson says the problem with this is that in the long run, and depending on other resources at their disposal, they are likely to run out of money, at a time when it is too late to do anything about it as they may be too old to get another job.

-

People are living longer. Once you reach 60, the average age of death for males is 79 and 84 for females. The longer you live the more money you require. Many more people live into their 90s and will need more money.

The above problems are then compounded by:

-

The age at which you retire. Early retirement means loss of income and further savings and the loss, if you are employed, of other service benefits. Of those surveyed, about 50% of members retired on the normal retirement date, 36.5% retired early and 14.95% retired late.

The average age of retirement was 63 years for 2019.

A separate Alexander Forbes survey, Member Watch, in which more than one million contributing members were measured, shows that higher contributions and length of service are critical to securing a reasonable retirement income.

Anderson says that if you retire at age 65 rather than at age 55 you will almost double your replacement ratio, assuming you started savings at age 25 years.

Given current market conditions following Covid-19 and the Moody’s downgrade, delaying retirement and staying employed for longer on a full or part-time basis, if possible, may be a good approach.

In 2019, the average contribution rate was 14.44%, but most of this (9.14%) came from employers. Legislation was recently passed which allows you to increase your contribution (from yourself and employer) to 27.5% of your taxable income (not your basic salary as with the Alexander Forbes survey), up to a maximum of R350,000 a year.

And if you do not cash in retirement savings along the way you will have a much better target of a financially secure retirement.

Inflation for retirees typically goes up above the average inflation rate. The reason is medical aid, where the rate of inflation is higher than average inflation. You will spend an estimated 60% of money on medical claims after you turn 60. The result of earning too little as a pension means that many pensioners are dropping out of medical schemes or downgrading to a lower option at the very time they need it most.

Anderson says that the most important things are: start saving early, build up an emergency savings of between three and six months’ income for tough times alongside your retirement savings, don’t withdraw your retirement money along the way, invest your retirement savings in an appropriate and diversified growth strategy when you are young, ensure you manage your expenses in retirement and do not make high-risk investments at retirement given that this capital is to provide an income for life.

You should also get financial advice before you retire.

If, when you are working, you think seriously about your pension, you will avoid the risk that many pensioners of private pension funds face of their income running out and having to live on the state old-age pension of R1,780 a month. DM

Over the next number of weeks a series of reports written by Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, will cover research undertaken by Alexander Forbes on retirement income in South Africa. Bruce Cameron is author of the best-selling book, The Ultimate Guide to Retirement in South Africa.

Contact Ascor®Independent Wealth Managers for retirement planning advice.

![]()

2 thoughts on “The capital of South Africa’s retirees is abysmal”

Comments are closed.